Payroll Savings – a brief guide to the simplest financial wellbeing benefit you're not offering yet

Reading time: 7 minutes

Perhaps your company offers private healthcare. Maybe a cycle-to-work scheme, an EAP, perhaps a few wellbeing app subscriptions. These are good benefits – but they address symptoms. They don't address the cause.

The cause, for most UK employees right now, is money. And the most effective, most requested, and most underused financial wellbeing benefit in the UK is one that 93% of employees love once they have it – yet only 7% of UK employers currently offer.

It's Payroll Savings. And it might be the easiest win your people team will ever find.

The problem you're already paying for

Financial stress doesn't stay at home. It walks into your office – or logs into your systems – every single day. And it is costing your business in ways that are rarely calculated but entirely measurable.

83%

of UK workers took at least one day off last year due to stress linked to personal finance – 61% took four or more days

(Workplace Wellbeing Professional, 2026)

£120bn

(4% of payroll)

estimated annual cost to UK businesses from lost productivity caused by employee financial stress

(PWC research)

59%

of employees say financial stress prevents them from performing their best at work

(HR Hub)

2.24 hrs

the average time employees spend dealing with personal finances during working hours every month

(Stream research, 2026)

These aren't edge cases. Nearly all workers (92%) have faced financial stress in the past year, with 89% reporting a direct impact on their work. Almost half say they find it harder to focus; a quarter say it actively reduces their productivity.

And despite this, financial wellbeing remains one of the most underprovided areas of the employee benefits package. Many HR teams know the problem exists. Fewer know what to do about it practically.

37% of employees say they want the option to save directly from their pay. That preference ranks above financial education, adviser access, and budgeting apps combined. (Stream, 2026)

What is Payroll Savings?

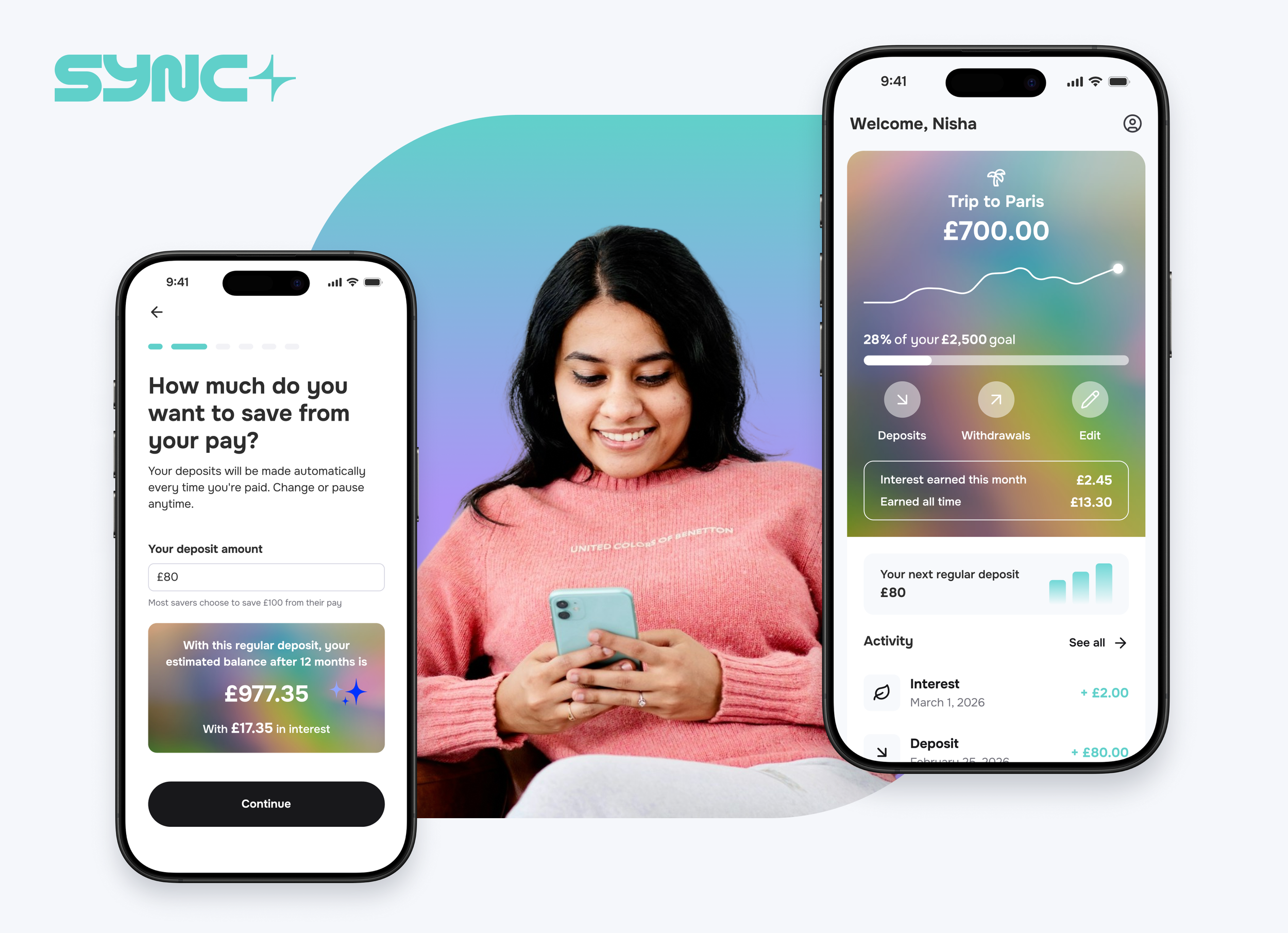

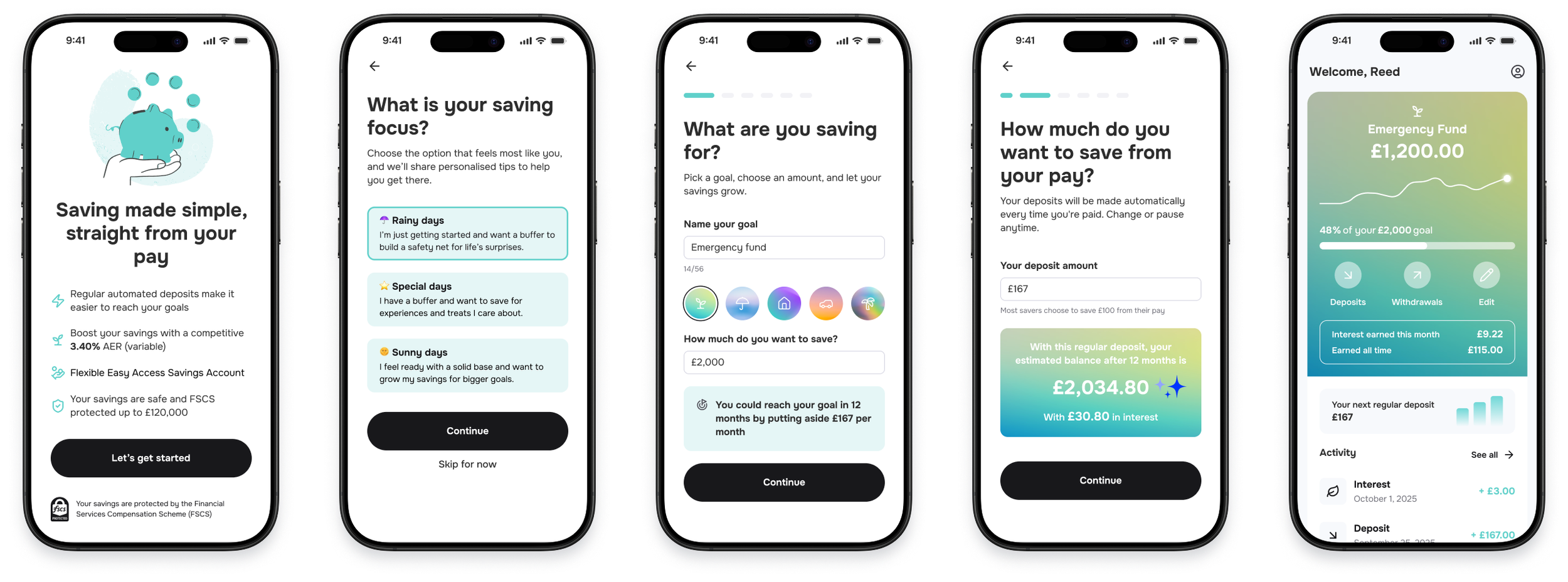

Payroll Savings is exactly what it sounds like: a fixed amount is automatically deducted from an employee's salary each month – before it hits their bank account – and deposited into a dedicated, high-interest savings account that they own and control.

Think of it as auto-enrolment for everyday savings. Just as workplace pensions use behavioural science to make long-term saving the default, Payroll Savings applies the same logic to liquid, accessible savings – the emergency fund, the rainy-day pot, the financial buffer that transforms how people feel about money day to day.

In a recent trial of an opt-out Payroll Savings setup, 93% of workers said they liked the scheme – whether or not they chose to save. A Co-op and Bupa trial found that an opt-out approach drove 70% active participation among colleagues. (Money and Pensions Service / Nest Insight)

The key features that make payroll savings so effective:

Automatic. The saving happens before employees see the money – so it never gets spent.

Accessible. Unlike a pension, employees can withdraw their savings whenever they need them. There's no lock-in, no penalty.

High-interest. With Sync Savings, employees earn a competitive rate from day one – significantly better than most high-street current accounts.

Flexible. Employees choose how much to save, can change the amount, or pause at any time.

Scalable. Works for employees at every pay grade – from entry-level to senior leadership.

The business case: what employers gain

This is not just a wellbeing initiative. It's a business investment with measurable returns.

➡️ Retention

Replacing an employee earning £25,000 or more costs an average of £30,614 – factoring in recruitment, onboarding, and lost productivity during the gap (Oxford Economics). Legal & General's workplace savings research found that companies offering Payroll Savings programmes saw a 12% improvement in employee retention rates.

83% of employees say they would be more likely to stay with an employer that provided financial wellness programmes. In a competitive hiring market, Payroll Savings is a genuine differentiator.

➡️ Productivity and absenteeism

Yorkshire Building Society's research on Payroll Savings found that implementing a scheme produced a 22% reduction in employee financial stress and a 17% decrease in absenteeism. Happy employees are demonstrably more productive – research consistently shows a 20% productivity premium for financially secure, engaged workers.

Nationwide Building Society reported a 45% reduction in employees seeking hardship loans and a 30% drop in salary advance requests after introducing Payroll Savings – both of which carry significant administrative cost.

➡️ Employer brand and recruitment

Financial wellbeing is now a recognised pillar of the overall wellbeing agenda, alongside mental and physical health. Employers who visibly invest in it attract candidates who are looking for more than salary. It signals that your organisation understands what employees' lives are actually like – and that it has their back.

Here's what financial stress is costing your business, and what Payroll Savings does about it.

💸 Financial stress – lost productivity, absenteeism, presenteeism → 22% drop in financial anxiety with Payroll Savings (YBS)

🔄 Staff turnover – £30,614 average cost to replace one employee → 12% retention improvement for employers offering Payroll Savings (Legal & General)

🏦 Hardship loans / salary advances – administrative burden, reputational risk → 45% reduction in loan requests after introducing Payroll Savings (Nationwide)

😶🌫️ Low engagement – disengagement costs UK employers £340bn every year → Financially secure staff are 20% more productive

🎯 Recruitment difficulty – roles unfilled, productivity gaps, rising hiring costs → Payroll Savings is a genuine differentiator in a competitive benefits market

What Sync Savings offers your employees

Sync Savings provides two products through the employer payroll channel – one that builds an immediate liquid safety net, and one that builds long-term wealth. Both are accessible to all employees, regardless of salary level.

1. High-interest Payroll Savings account

Our core Payroll Savings product gives every employee a dedicated high-interest savings account, funded automatically from their payslip. No apps to download first. No direct debits to set up. No decisions to make every month.

Savings are fully accessible – employees can withdraw at any time, with no penalty. But because the money leaves the payslip before they see it, the behavioural science works: people keep more saved than they ever would by transferring manually. Savings are FSCS protected up to £120,000, for complete peace of mind.

For employees at different salary levels, even a modest monthly deduction builds meaningful financial resilience within a year:

Entry level (£22k) – saving £50/month → ~£600 + interest after 1 year / ~£1,900 + interest after 3 years

Mid-level (£35k) – saving £150/month → ~£1,800 + interest after 1 year / ~£5,600 + interest after 3 years

Senior (£60k+) – saving £300/month → ~£3,600 + interest after 1 year / ~£11,200 + interest after 3 years

Use our savings calculator to see what your team could build.

2. Stocks and shares ISA – for long-term wealth

For employees who want to go further than a savings account, Sync Savings also offers access to a stocks and shares ISA – available directly through the payroll channel.

This allows employees to invest up to £20,000 per year (2024/25 allowance) in a tax-efficient wrapper, with all growth, dividends, and income completely free of UK tax. Unlike a pension, there's no minimum age for withdrawal – employees retain full flexibility.

Offering ISA access through the payroll channel positions your business at the leading edge of financial wellbeing provision – and gives employees a genuine long-term wealth-building tool, not just an emergency fund.

How it works: simple to implement, easier to run

One of the most common objections we hear from HR and payroll teams is the fear of complexity. Payroll Savings sounds like it might mean new systems, new admin, new liabilities.

It doesn't. Here's how implementation with Sync Savings actually works for employers:

1. Initial setup

We connect directly with your payroll provider. Most integrations are live within two weeks. No new software for your team to learn.

2. Employee enrolment

We handle all employee-facing communication, onboarding, and account opening. Your HR team doesn't carry the admin load.

3. Monthly deductions

Agreed saving amounts are deducted via payroll – exactly like pension contributions. Your payroll team makes one additional line entry.

4. Ongoing management

Employees manage their own accounts, contribution levels, and withdrawals directly through the Sync Savings platform. You're not involved in day-to-day activity.

5. Reporting

You receive regular insight on participation rates and aggregate financial wellbeing metrics – useful for board-level ESG and people reporting.

There is no requirement for employers to make matching contributions (though you can if you wish). The cost to offer the scheme is low – and the business case in productivity, retention, and recruitment pays back many times over.

Only 7% of UK employers currently offer Payroll Savings to their teams – despite the FCA, the Money and Pensions Service, and the Government all actively encouraging wider adoption. The employers who move now will lead. (FCA, 2024)

Is this right for your organisation?

Payroll Savings through Sync Savings is designed for any UK employer with a regular payroll and offers Universal Access for all employees. It works particularly well for:

Employers with a diverse workforce including part-time and lower-income workers who are least likely to have existing savings and most likely to be affected by financial stress.

Organisations with financial wellbeing gaps in their benefits stack – strong on health and mental wellbeing but with little direct financial support.

Businesses with high turnover looking for a tangible, low-cost benefit that improves retention.

HR teams under pressure to demonstrate ESG or people strategy credentials – Payroll Savings is measurable, reportable, and genuinely impactful.

Forward-thinking employers who want to be ahead of what is likely to become an expected benefit within the next few years, not a differentiator.

Start the conversation

The data is clear. Employees are financially stressed. They want help. They want it through payroll. And the employers who respond to that – with something practical, automatic, and genuinely useful – will be rewarded with a more focused, more loyal, and more productive workforce.

Workplace savings won't replace a pay rise. It won't solve every financial challenge your employees face. But it is the single most impactful, most requested, and most overlooked financial wellbeing benefit available to UK employers today.

And with Sync Savings, it takes two weeks to go live.

Talk to our team about how we can integrate Sync Savings with your payroll system – and what your employees could start building from their very next payslip.

Sources

Workplace Wellbeing Professional (2026) | PWC Employee Financial Wellbeing Survey | Stream Workplace Finance Research (2026) | Money and Pensions Service / Nest Insight Payroll Savings Trials | FCA Financial Lives Survey 2024 & Workplace Savings Statement | Legal & General Workplace Savings Study | Yorkshire Building Society Payroll Savings Research | Nationwide Building Society Payroll Savings Data | Oxford Economics Cost of Employee Turnover | HR Hub Financial Wellbeing Survey | CIPP Payroll Savings Guide

This content is intended for UK employers and HR professionals and does not constitute financial advice.